‘Consumer Confidence’ is a contentious construct, subject to multiple views and versions on how it should be measured. The predictive power of a Consumer Confidence Index (CCI), at the macro and micro levels, is also given to argument. Yet measures of consumer confidence are applied in economic discourse as a useful indication of ongoing consumers’ attitudes towards the economic situation in their country and their own wellbeing. It may tell where consumers think the wind blows by tapping consumer sentiment of optimism versus pessimism.

At the base of a metric of CCI are four measures most commonly used; conceptually they elicit four comparisons:

- How do you think the economic situation in your country today compares with X months ago?

- How do you think the economic situation will be in X months from now compared with today?

- How would you describe the state of your finances / standard of living today compared with X months ago?

- How do you expect the state of your finances / standard of living is going to be in X months from now compared with today?

The comparisons requested often span a period of six months or a year (i.e., X = 6 or 12). The assessment answers are basically ‘better’, ‘the same’, or ‘worse’ (e.g., using a short 3-point item scale or a more detailed 5-point item scale). The four measures can be summarised in a 2×2 matrix: time reference {past, future} by level of reference {national, individual}. However, metric indicators of CCI may be expanded by research agencies to include consumers’ views or expectations in specific areas such as the job market, equity investments, and spending on durable products or on discretionary goods and services (e.g., holiday travels). The metrics also differ in how they are calculated.

Changes in CCI values over time may give an indication of expected decreases or increases in consumer expenses and spending from the consumers’ perspective; this should reflect in projections of companies’ sales and revenues. The ability to predict macro economic events (e.g., expansion or recession) with CCI is in greater dispute. Theoretically, increased consumer spending, driven by expected improvement in the economic conditions or furthermore one’s own finances, would contribute to expansion (i.e., domestic consumption is a primary engine of GDP growth), and vice versa. But corroborating these relationships with data (e.g., for anticipating recessions) is elusive. That is perhaps why some researchers prefer to highlight the objective of their metrics as measures of ‘consumer sentiment’. Still, sentiment or confidence can be important as expressions of consumers’ expectations and mood, whether they see themselves going into a more positive or negative period, which might direct their behaviour in coming months (e.g., embark onto a shopping spree or tighten up the household budget).

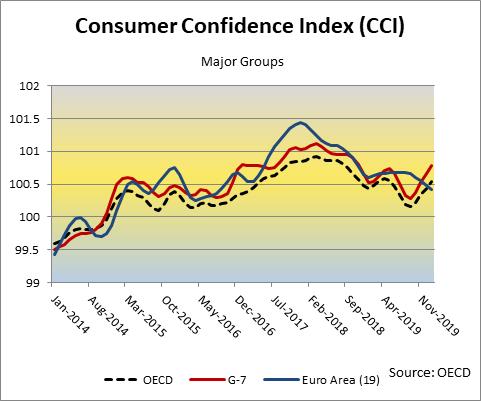

Trends and implications of consumer confidence are demonstrated below by means of the metric of CCI by the Organization for Economic Cooperation and Development (OECD) for major groups and selected countries. First, the OECD is a widely recognised and respected international organization with a strong research arm (its statistical indices are regularly used as rulers and benchmarks by member countries in multiple fields). Second, the CCI of the OECD makes it possible to compare countries on the same measure of consumer confidence over time.

As explicated by the OECD, its Consumer Confidence Index “provides an indication of future developments in households’ consumption and saving, based upon answers regarding their expected financial situation, their sentiment about the general economic situation, unemployment and capability of savings” (OECD Data, CCI). In the charts presented below, a ‘baseline’ of 100 marks a long term average (amplitude adjusted) between January 2014 and January 2020. Index values above 100 indicate a ‘boost’ in consumers’ confidence about the forthcoming economic situation which may translate, for instance, into inclination to spend more money on major purchases during the next 12 months (consumers are presumably in a more positive mood). Conversely, values of CCI below 100 indicate a pessimistic attitude towards future economic developments, which may lead consumers to consume less and save more (consumers are probably in a more gloomy mood).

- Source of data for the three charts below: OECD (2020), Consumer Confidence Index (CCI) (indicator). doi: 10.1787/46434d78-en (accessed on 24 February 2020).

Ever since the second half of 2014 consumers in countries of the OECD felt more positive about the economic situation, and for almost all that time to the beginning of 2020 consumers resident in the stronger G7 countries as well as in the Euro (monetary) Area expressed greater confidence and optimism than in the OECD as a whole. The situation in the Euro countries must have seemed particularly positive and encouraging during 2017, but then came a big slump throughout the following year — social tensions and political instability inflict several of the member countries. Most recently (since September 2019), the Euro Area’s economic mood appears to be going in an opposite direction to the G7 (Germany, France and Italy are in both groups, the UK is part of G7 but not the Euro block, and starting from February 2020 not in the EU either).

For a while Euro Area residents were optimistic about the outcomes of efforts and reforms to heal the countries in deep debt and to push ahead the EU economy following the recession of 2008-2012, but seemingly that did not work out to their expectations. Now they could be feeling disappointed to the extent of disillusioned — with caution warranted, this is not a good sign. Expectations about a new recession have been raised since early 2019 but it has not happened (yet); without rushing to make predictions based on any downturn in consumer confidence, we should be alert to the warning signs from Europe, especially if we consider the whole period from 2018 to the start of 2020.

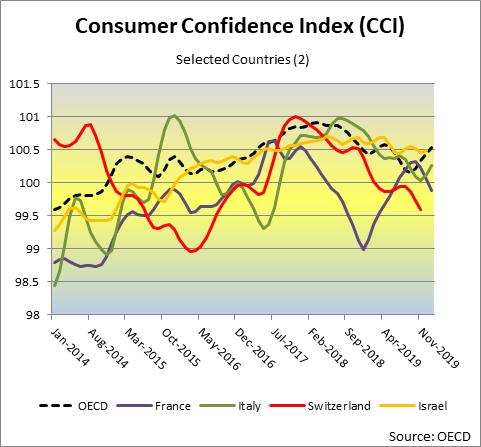

In 2015 things seemed to be going just right in Great Britain; Cameron won the elections for the second time, and the people of Scotland rejected the motion for independence from the UK (positive events for the economy). Then came the initiative of a referendum for Brexit, the departure of the UK from the EU. All through 2016, from the months preceding the referendum (June 2016) until just after it took place, the CCI took a deep dive (a whole point of CCI), and stayed lower. It was still above the OECD average and in the ‘positive zone’ for some time, but fluctuations continued in the next three years, which coincide remarkably well with stages of the turbulent process of approving Brexit in the political system, with two elections in-between. British consumers, burdened by high uncertainty and bitter skirmishes with the EU, were largely unhappy during a period when consumers in other OECD countries felt mostly more positive. This somber atmosphere likely did not help to recuperate the ailing retail sector. New hope is finally on the rise following the elections won by Boris Johnson and the Conservatives in December 2019, and the formal execution of Brexit thereafter — much depends from now, of course, on whether negotiations with the EU lead to an amicable agreement.

In Germany, the main political and economic power in Europe, consumers’ sentiment improved for nearly two years, from early 2016 to late 2017; there was probably a feeling that the financial crisis and its effects were dissipating. But then the ascend was broken, followed by (almost) a continuous decline in CCI, reflecting a worsening mood. This trend may be attributed mainly to discontent over the immigration crisis and the planned resignation of Chancellor Angela Merkel from political life, announced by her in the end of October 2018. Consumers raised their concern due to these developments, with possible negative effects on the political as well as economic situation in the country.

In the United States, however, it would seem that the economic situation could not be better since President Trump was elected and going on during his (first) term in the White House. Looking a little backwards, we can notice that the American sentiment climbed out from the ‘negative zone’ already in 2014 towards the end of Obama’s presidency. Consumers’ confidence looks ‘jumpy’, and yet the CCI has been hiking again just recently, since the summer of 2019. Unemployment is at its lowest level for years and the economy is strong — the Americans seem overall pleased. In this state of affairs, one may wonder about the prospects that the Americans would want to replace Trump.

The ups and downs in consumer confidence in France and Italy reflect the socio-economic and political turbulence in those European powers. The peaks and lows in Italy are more dramatic throughout the past six years, showing greater nervousness of the Italian consumers — the Italian economy remains at risk, its debt issue is still not satisfactorily resolved, and the governments are far from stable.

In France things were going quite well for the consumers, as suggested by the CCI indicator — until President Emmanuel Macron came to power in the spring of 2017. His reforms seem to have turned the French consumers more nervous and suspicious about the economic conditions in their country, and probably in particular about their personal financial situation and wellbeing. The strong response to Macron’s first wave of reforms (e.g., loud protests on the streets) is mirrored in a sharp decline of 1.5 points in CCI during 2018. After Macron started to soften his plan, the consumers started to think more positively again in 2019, and CCI returned above 100. But since October 2019 Macron’s insistence on his pension reform is pushing the confidence or sentiment of the French downwards again. However necessary are the reforms of Macron for the health of the French economy, the consumers do not welcome them.

What seem even more surprising are the ‘hills’ and ‘valleys’ in confidence of the Swiss consumers. It shakens the image of Switzerland as a bastion of safety and stability. Nevertheless, being nestled between Germany, France and Italy, Switzerland is not really isolated and probably could not remain unaffected by events in its neighbouring countries and the EU as a whole, given also that its economic ties with the EU have become even stronger. There are additionally internal issues that might trigger the changes in CCI observed in the chart above (e.g., troubled and weaker banking system, rising costs of living, immigration, and other matters voted on in frequent referendums).

Compared with consumers in those countries, Israeli consumers might appear as an examplar of calm and stability. Their confidence in the economy gradually improved from January 2014 and until mid-2017, remaining relatively stable (a little ‘jittery’ but the situation is perceived largely ‘the same’) since then, at a positive level of 100.5. The Israeli consumers appear overall pleased about the economic situation in the country and content with their ability to continue shopping as usual, presumably making many of them less motivated to unseat the incumbent Prime Minister, Netanyahu, in power for the last decade.

(Note: Values of CCI for Switzerland in December 2019 and values for Switzerland and Israel in January 2020 were still missing.)

Up until January 2020 the CCI indicators probably do not account yet for the outbreak of the Corona virus disease (COVID-19) worldwide and its impact on the economy as already seen. Anticipating values of CCI to drop from February, consumers would become more worried and cautionary, and less likely to engage in shopping and money spending. On the other hand, there is an opposite stance that suggests that consumers in a somber mood would try to compensate by shopping more; if they are still worried about going to public places like malls and large stores, it is plausible that we will see an increase in online orders made from their homes.

The concept of consumer confidence blends economics with psychology. It is about the mindset of consumers, their attitudes, expectations and mood regarding the economic situation at the national and individual (household) levels. Even though the vast majority of consumers are not experts in economics or finance, what they think and feel about economic developments, as crucial agents in markets and the economic system at large, can be critical factors in shaping their spending and consumption behaviours.