Countries face several economic challenges while they are trying to recover from the coronavirus pandemic: recuperating the economy from a traumatic recession (shock-induced shutdown and negative growth); increased budget deficit, possibly leading to larger debt; combatting high (and stubborn) unemployment, together with changes in the job market. But reigniting the economy might be tied with another challenge of avoiding price rises from spiraling out of control into an inflationary process. As people are pushing to resume normal business, commercial and consumption activities, there is a risk that the economy will heat up, pushing consumer prices to rise at higher rates. The recovery process, therefore, has to be moderated, and if needed, slowed down (e.g., by increasing interest rates). Certainly every step taken has to be watched carefully for its impact on each of the economic and social factors, yet price rises have to be monitored attentively lest they could transform into inflation with potential devastating effects.

Is there a reason to worry in sight about consumer prices? Is inflation really lurking? Temporary ‘hikes’ may represent market price adjustments whereas inflation is characterised by steady and continuing price increases (they may start mildly and then accelerate). This post inspects the Israeli case.

From January to May 2021 the consumer price index (CPI) in Israel rose 1.5%; in the last twelve months, by comparison, the CPI also rose by 1.5% (May year-over-year) — that is, by the end of May 2021, within five months, consumer prices have already risen by the same rate of a year. According to a trend projection (based on the pace in the period February-May 2021), the Central Bureau of Statistics (CBS) in Israel forecasts an annual rate of 2.4% increase of CPI [1]. In 2018 and 2019, before the pandemic erupted, CPI increased by annual rates of less than 1%, whereas in 2020, a year inflicted by lockdowns and business shutdowns for more than six months of the year, the annual rate was negative (i.e., prices dropped).

From here on, comparisons will be based on CPI excluding housing (i.e., rentals, costs incurred by owners) to avoid effects associated with the real-estate market. The aim hereby is to focus on typical and current consumption activities and expenses. The price index covers goods and services, and durable as well non-durable goods.

The trend projection of annual rate increase for CPI excluding housing is also 2.4%. In the past five years, the year-over-year changes in consumer price index excluding housing (denoted hereon CPIndex) for May were as follows:

| 2017 | 2018 | 2019 | 2020 | 2021 |

| 0.5% | -0.1% | 1.2% | -2.6% | 1.7% |

- CBS also reports on changes in CPI excluding fruits & vegetables because of their relatively large fluctuations and seasonality effects, but they are considered to the purpose of this discussion as essential consumption spending. Note that house maintenance costs (e.g., repairs, renovations) and services (e.g., utilities: water, electricity, gas) are not part of the category of ‘housing’ and hence are included in CPIndex used here.

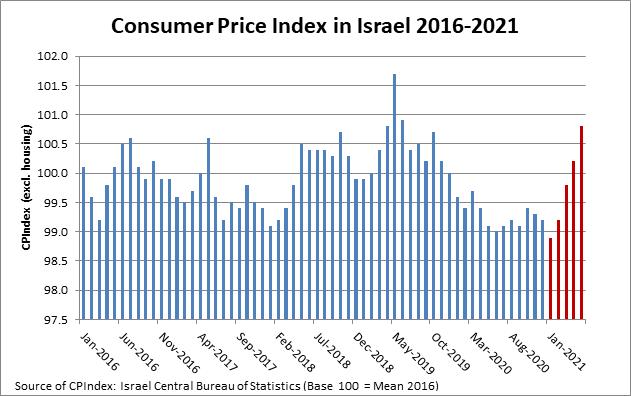

The phenomenon about CPIndex that attracts attention is the steep climb since January 2021 as can be seen in Chart 1 (notice columns in red). This climb is quite distinctive from the levels of CPIndex in the previous year of 2020. The year 2019 seems to stand out in exhibiting higher index values (note the peak in May 2019). At the very least we might see in the rising prices of early 2021 a sign of recovery in markets activity, similar to levels in previous years.

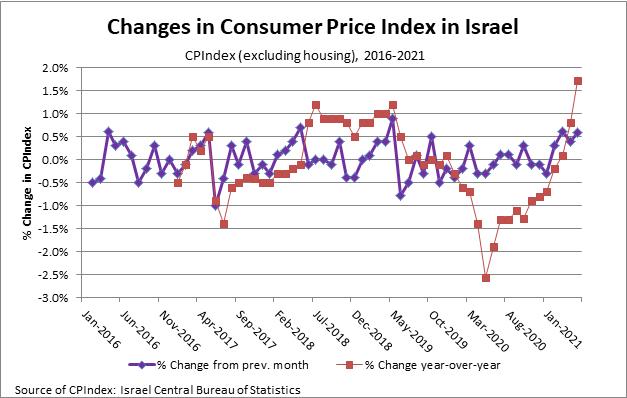

The changed direction in price levels is also reflected in monthly changes in CPIndex as shown in Chart 2 (line in purple). From February to May 2021 — for four months in a row — the CPIndex increased (~0.5%) from the previous month, a situation not seen since mid-2019. It is hard to detect systematic highs and lows in specific months (seasonality effects of different products and services seem to be confounded in the integrated price index). Consequently, there is little reason to expect that prices overall will drop in the second half of 2021, offsetting the increases of the first half. The monthly increases are also mild at this stage.

Therefore, we may find more indicative signs in the annual changes, year-over-year for same months, in the CPIndex (red line). The hike, or rather resurrection, in prices since February 2021 could be concerning. Actually we can see how gaps start to narrow down already from October 2020, although the price levels until January 2021 are still lower than in the previous year, respectively. (Between October 2020 and February 2021 Israel was going through a second wave, then a third wave of COVID-19 as vaccination was progressing) The deepening falls in CPIndex from December 2019 and then the run upwards from May 2020 are a cue of the instability of the pandemic period. The rise in prices is not quite corresponding with the pace of recovery (e.g., in terms of GDP growth) which is still unstable and lingering [2]. It is especially the momentum of prices pushing upwards that raises concern.

This rise may be only temporary, an outcome of the effort to get the economy on its feet again, and we should not be alarmed because of it. The development that worries about this rise in price level is the atmosphere that is building up in the country of raising prices. Manufacturers and retailers are announcing that prices are about to go up, and some have already declared price increases of various products. Firms are telling consumers that they should expect prices to rise until the end of the year. A group of restauranteurs, which was formed during the COVID-19 crisis to defend their businesses, published a call recently that suggests justifications for raising their prices to diners at this time. This call in particular attracted attention because it invoked suspicion of signalling a coordinated move to raise prices (this matter is currently under enquiry of the state Competition Authority). But there is overall a flurry of prior announcements and actual price raises that seems intent on giving legitimacy to raising consumer prices. The risk in nurturing expectations for price increases is the tendency of expectations to materialise (i.e., people follow their expectations), and single rises in price level that accumulate may turn into an inflationary process.

- Update (December 2021): A new concern emerged recently, apparently even more serious than the restaurants’ affair, whereby a number of leading retailers (supermarket chains) and producers in the food and grocery categories are suspected of giving signals of price increases through public announcements, and covertly engaging in price co-ordination between them; this matter is also now under investigation.

On the demand side, consumers return to shopping and buying in stores more frequently and expediently, perhaps in an attempt of compensating for lost time (e.g., purchases planned that had to be deferred). Offline purchases in physical stores add-up again to online purchases. The heightened demand avails companies to raise their prices to consumers, but it may also lead markets to over-heat and lose their brakes on prices. However, on the supply (cost) side there also are some factors that may sustain price increases: shortages in consumer products caused by (labour) disruptions to production, continuing shortages reportedly in raw materials, but most of all increased costs of transportation (mainly in sea). Both demand and supply forces may keep prices going up for a while.

Lastly, we will look at prices in two categories of expenses: (a) dining in restaurants and coffee houses; and (b) guest accommodation, recreation and trips (i.e., taking vacations). These categories also represent types of leisure activities. While they are not essentials, participating in these activities, and spending money on them, symbolised for many consumers lately a fulfillment of their desire to resume previous lifestyles, entertain and enjoy themselves again after a difficult period, and taking a break to loosen up and refresh away from home on vacations.

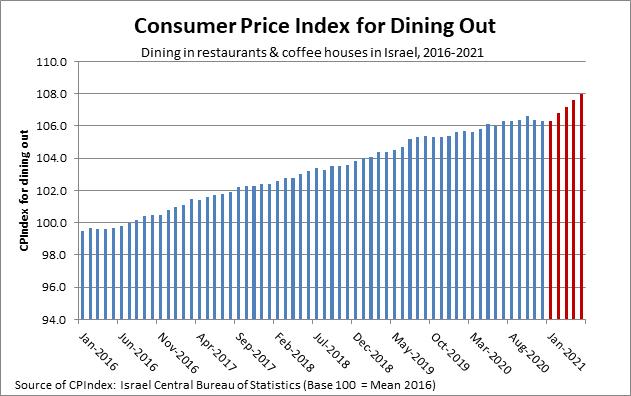

Dining in Restaurants & Coffee-houses (Chart 3): From the beginning of 2021 we can see a steep climb in price index for dining out, which looks like prices are breaking away from a ‘quiet period’ of previous year. But if we go backward, one finds that prices were going up steadily from mid-2016 to mid-2019: in these years the CPIndex for restaurants and coffee houses was increasing at a compound annual growth rate (CAGR) of 1.6%. Only in 2020 this climb was slowed down following restrictions of COVID-19 that forced restaurants to shut down or operate on basis of take-away orders for much of the year. Hence, the renewed rise in prices should not surprise consumers too much — the restaurants and coffee houses are returning to a pace of pre-Corona era (annual rate, year-over-year, of 1.5%-1.8% in March to May). It is only a modest rate of increase, but precisely because it can continue so long and steadily, it is discomforting — and what it might tell consumers about prices for dining out in the coming months.

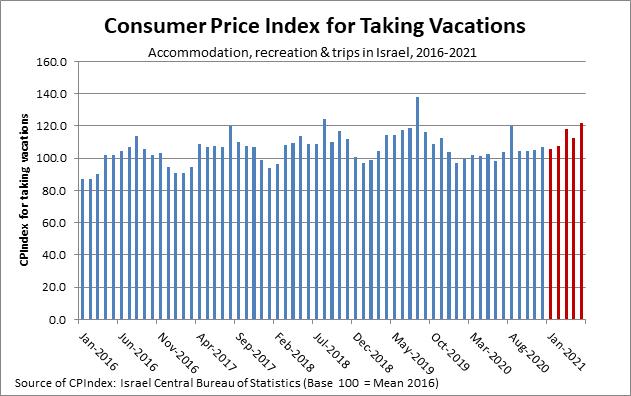

Taking Vacations; Accommodation, Recreation and Trips (Chart 4): Prices for taking vacations in the country reveal a clear seasonal ‘summer’ effect, when more Israelis take time out, especially families with children. The CPindex for accommodation, recreation and trips is higher between April and November (warmer months), and is at its peak in August. The CPIndex for this category reached its highest peak in five years in August 2019. Last year, 2020, was different, without the usual ‘hill’ shape over the period April-November, but even then August exhibited higher prices — Israelis were not giving up on their holidays so easily (there was also a relief from COVID-19 that summer). As for 2021, we can see a revival of the pattern of previous years, pre-Corona. In May the price index in this category rose 8.5% from April, making it a major contributor to change in CPI overall (0.4% [1]). The prices in 2021 already appear to be higher than in 2020, indicating a revived interest of Israelis in vacations (e.g., in May the price index was 18.5% higher than its respective in May 2020) — how high will it get by August, compared with 2020, or 2019?

It is hard to determine yet how far and how long the rise in CPIndex of early 2021 will continue through the second half of this year. It could still be halted (or postponed) by another wave of the coronavirus (caused by a new variant like Delta). Based on the past few months, the annual increase in consumer price index for 2021 is expected to be higher than in the past five years, but it is still a slow pace. It does not seem that Israel is nearing inflation at this time. Nonetheless, policy makers should not overlook existing factors or signs that may lead to development of an inflationary process. The possibility that inflation is lurking around a corner cannot be excluded; it would be complacent to assume otherwise.

Sources:

[1] Press Release on Consumer Price Index (Hebrew), Central Bureau of Statistics (CBS) in Israel, 15 June 2021

[2] Press Release on Growth in GDP (Hebrew), Central Bureau of Statistic (CBS) in Israel, 16 June 2021

[*] The data on consumer price indexes for the charts were extracted with CBS online generator of data series of prices and price indexes.

I throroughly enjoyed this lucid analysis about the recent hike in prices. Dr. Ventura manages to shed light on the underlying reasons.

LikeLike